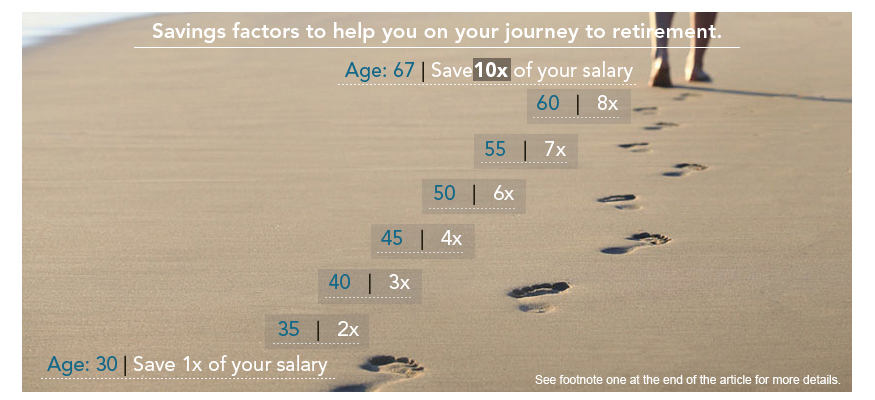

"By 35, You Should Have Double Your Salary Saved" - Do You?

- Thread starter BWoog

- Start date

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

People here confused with owning a house and not having so much savings... oh jesus just count the house in, how much did you invest in that? It's not like it's money lost if it didnt somehow go down in value a lot. How hard can this be?

like "I put a 50k down payment on my house so I got nowhere near 2x my salary in savings lul"

like "I put a 50k down payment on my house so I got nowhere near 2x my salary in savings lul"

37 and yes, absolutely. If I combine my retirement plan and the stocks I've bought "manually" it comes out to more than double my yearly salary.

No kids, no car, no house, relatively cheap apartment. Makes it dead easy to save up.

No kids, no car, no house, relatively cheap apartment. Makes it dead easy to save up.

I'm 33 and have pretty much my salary saved. Double? I'd need to start doing additional deposits into my super...3 years ago

People here confused with owning a house and not having so much savings... oh jesus just count the house in, how much did you invest in that? It's not like it's money lost if it didnt somehow go down in value a lot. How hard can this be?

like "I put a 50k down payment on my house so I got nowhere near 2x my salary in savings lul"

I don't think equity is included but I could be wrong... Though it probably should be, If that's the case I think a lot more people would feel a lot better and me personally would probably be on track to hit that magic 2x number.

Edit: actually on second though if equity isn't included that's a big factor that changes for a lot of people.

Yes, people that meet these metrics will have most of the money invested in 401k/IRA/Roth IRA/brokrage etc. Not savings. It is supposed to be savings invested. If it is sitting in cash/low interest savings, it is losing purchasing power over the years.So I've got a year to save up $100k.

Well I'm on the right track. I have like $5k in the bank.

Does my 401k count?

What kind of fucking medical school is this that you were that desperate to apply to? Average debt for a 2017 grad is expected to be right around $200K.

Plus bachelors, plus masters, plus interest compounded per annum at 6%

And all said debt in a large, expensive city:

https://www.usnews.com/best-graduate-schools/top-medical-schools/debt-rankings

Both my wife and I had grad school so had a bit of a slower start. That said, it was worth it. We now how have a high income so double will take awhile, but we'll have it by late 30s easy.

Even if rent = mortgage, the argument is that the gains you get by investing the down payment, property tax, and maintenance costs will be the better investment in the long run, but yeah, the area you live in is a very important factor along with interest rates. But a mortgage investment should not be made based on wanting to own a home as soon as possible.Don't forget that if you don't own, you still have to pay rent money to live somewhere, which is entirely lost money. While you aren't paying much towards the principal when a mortgage is initiated, the amount added to the principle each month grows over time and adds up.

There's a NYT calculator that does a good job of telling you whether renting or owning is better. It mostly comes down to the cost of owning versus renting in the area you live in.

https://www.nytimes.com/interactive/2014/upshot/buy-rent-calculator.html

Even if a couple is planning ahead and gets a mortgage for a 3 bedroom house, it's unnecessary early in life. That's investment money that should be making you more money, not making your mortgage bank money.

When you rent, it's easier to upsize when you have to and easier to relocate when want or have to without being at the mercy of the real estate market at the time. Renting also provides a better opportunity to save and invest because in most cases it's going to be cheaper to rent than own + mortgage.

Everybody wants to own a home, I get that, but in my experience it's much better to wait. Rent and compound invest early in life so you can save up a huge down payment for a short term mortgage. You have the movement flexibility that renting provides, and you are avoiding the long term mortgage debt, which are incredible rip offs IMO.

Ultimately the best plan would be to save and invest enough to buy a house outright and avoid interest payments entirely, but that's obviously not going to work for most people. Although it happens a lot more than people think. Smart and diligent investing adds up fast when you start investing early and often.

Banks want you to go into debt. They want you to get a long term mortgage. They want you to do this because it makes them an incredible amount of money. That's interest money that you should be investing for your future, not theirs.

I'm pretty close to 30 and I have pretty close to my annual salary in my retirement account. Planning to increase my retirement contributions by 1-2% annually for a few years once I turn 31, just to add a little bit of insurance in case my account would otherwise lag a little behind the "2x income by 35" goal. Since my wife's a teacher, she's on a pension plan that we'll start supplementing soon with a Roth IRA or something.

Some people would probably suggest I grow my contributions now, but right now I don't really have a rainy day fund I'm comfortable with, and I'd like to have more free cash on hand. My regular savings aren't exactly terrible, but now that I own a home I'd like to be a little more prepared for sudden expenses. We've gone through a string of setbacks already this year and it's been tough to recover from them and resume saving at the level we were at the start of the year.

Once we hit our arbitrary emergency savings goal, we're gonna pay down our auto and student loans, then shift all our extra savings to retirement savings. It's gonna be great.

Some people would probably suggest I grow my contributions now, but right now I don't really have a rainy day fund I'm comfortable with, and I'd like to have more free cash on hand. My regular savings aren't exactly terrible, but now that I own a home I'd like to be a little more prepared for sudden expenses. We've gone through a string of setbacks already this year and it's been tough to recover from them and resume saving at the level we were at the start of the year.

Once we hit our arbitrary emergency savings goal, we're gonna pay down our auto and student loans, then shift all our extra savings to retirement savings. It's gonna be great.

It's crazy seeing how angry and upset people get over this type of stuff. Seems like people bitch about being in debt too, but don't do anything to get out of debt or think it's somehow normal(?).

I won't say that I'm not currently in some unsecured debt, but I will say that I've realized how bad of a financial decision it is to be in debt, and am working my way out of it as quickly as possible. I'm hoping to be able to double my current monthly savings in about a year and keep increasing it as I earn more.

Having no money to allow me to retire is an extremely scary thought, and I am so happy I realized how important it is to save at a relatively young age!

I won't say that I'm not currently in some unsecured debt, but I will say that I've realized how bad of a financial decision it is to be in debt, and am working my way out of it as quickly as possible. I'm hoping to be able to double my current monthly savings in about a year and keep increasing it as I earn more.

Having no money to allow me to retire is an extremely scary thought, and I am so happy I realized how important it is to save at a relatively young age!

I turned 30 in March and I have about 3.3x my annual salary saved between my 401k, Roth 401k, savings, checking, and money market.

No home equity since I rent. No debt, either .

Yay?

I'm gonna be just like you in 3.5 years when I'm 30, too!

I live in La. I didn't have any student debt though coming out of college so that helped a ton. That and rent was cheaper.

When did you graduate?

Even if rent = mortgage, the argument is that the gains you get by investing the down payment, property tax, and maintenance costs will be the better investment in the long run, but yeah, the area you live in is a very important factor along with interest rates. But a mortgage investment should not be made based on wanting to own a home as soon as possible.

Even if a couple is planning ahead and gets a mortgage for a 3 bedroom house, it's unnecessary early in life. That's investment money that should be making you more money, not making your mortgage bank money.

When you rent, it's easier to upsize when you have to and easier to relocate when want or have to without being at the mercy of the real estate market at the time. Renting also provides a better opportunity to save and invest because in most cases it's going to be cheaper to rent than own + mortgage.

Everybody wants to own a home, I get that, but in my experience it's much better to wait. Rent and compound invest early in life so you can save up a huge down payment for a short term mortgage. You have the movement flexibility that renting provides, and you are avoiding the long term mortgage debt, which are incredible rip offs IMO.

Ultimately the best plan would be to save and invest enough to buy a house outright and avoid interest payments entirely, but that's obviously not going to work for most people. Although it happens a lot more than people think. Smart and diligent investing adds up fast when you start investing early and often.

Banks want you to go into debt. They want you to get a long term mortgage. They want you to do this because it makes them an incredible amount of money. That's interest money that you should be investing for your future, not theirs.

It's complicated.

First, a 30 year loan here in Austin gives an interest rate of 4.3%. Annual inflation is 2-2.5%, so you're really only paying the difference. Which is tiny. In that sense I see a 30 year loan as very cheap.

Second, housing prices in many major cities are high now. So even with a great interest rate, you could find yourself having severely overpaid if the market goes into recession over the next 2 years, which there's a good chance of.

Third, the best I've seen of this is to NOT think of housing as an investment but a lifestyle choice. Especially with two persons involved it's really hard to make it a numbers game. And it's often an emotional thing. I've been there.

If

(1) you're in a LCOL or MCOL area where median house can be bought for 200-600k

AND

(2) you see yourself as having a high chance of staying in that area for at least 10 years

AND

(3) you have a job and can afford it

I think you should most definitely buy. I haven't bought as I have worked in 4 different countries in the past 10 years. But it's about time to settle down and I'll definitely buy even at these interest rates, which are historically low for the USA.

I'm 37, If you count equity then I am well over because I send a lot of extra money towards the principle of my mortgage and the value of the property is really high compared to what I owe. If I can save up to about 1x my salary again I would buy another house and just rent the first one. I am trying to not let extra money just sit in the bank anymore.

Totally understand the emotional thing. There are family pressures and societal expectations that everybody should have the 3 kids and the white picket fence and it's OK to want that, but you don't need to have all that before the age of 25.Third, the best I've seen of this is to NOT think of housing as an investment but a lifestyle choice. Especially with two persons involved it's really hard to make it a numbers game. And it's often an emotional thing. I've been there.

Mortgage interest rate were ridiculously high when I first bought. It was a big, big mistake for me to buy young. Now interest rates are good so a 30 year mortgage is worth a consideration but I still wouldn't recommend it. Even with low interests rates the overall cost difference between a 30 year mortgage and a 15 year mortgage is really significant. Waiting and investing for that eventual 15 year mortgage would definitely been the better choice for me.

That early lifestyle choice can have a big impact on the late lifestyle choice.

Don't get me wrong, based on pure numbers investing is the way to go. I just don't like the way the argument is presented as 4% interest vs 7+% as some kind of no-brainer. There are legitimate reasons why someone would want to pay off their home early instead.

Absolutely. A house with a mortgage on it is a leveraged asset. That exposes you to more deep risk than a normal investment would. It is possible for the value to go negative if the market value of the house falls below the amount remaining on your mortgage. Then you are between a rock and a hard place, because you now can't even move for new job opportunities without defaulting.

I would think this would be in everyone's financial calculus considering that it was part of a huge national crisis just 10 years ago, but it seems like many have short memories.

This seems to be primarily aimed at Americans, for whom I guess private retirement saving is kind of all there is?

Here in Sweden we have a public pension system, which is paid into every month by you and your employer. The total is 18% of your salary I believe, but only a few percent of that comes out of your salary through taxes. The largest part is paid by the employer as part of the employer fee. Is America's Social Security kind of this, or...?

In the US it is 12.4% for Social Security split evenly between employer and employee, but yeah, basically the same concept. It is a compulsory public pension system.

Including our work pensions, my husband has the 2x saved. I only have about 1x. lol

Anyway, if you're poor, you're poor and won't have money to save so this advice doesn't really count for you.

I think this advice is more for middle+ class working professionals who don't know what they are doing with their money.

That said, my husband and I are not professionals but we're trying our best and also wasting a bunch of money on the side, but maybe the healthcare situation in the US makes this even more difficult.

Anyway, if you're poor, you're poor and won't have money to save so this advice doesn't really count for you.

I think this advice is more for middle+ class working professionals who don't know what they are doing with their money.

That said, my husband and I are not professionals but we're trying our best and also wasting a bunch of money on the side, but maybe the healthcare situation in the US makes this even more difficult.

Including our work pensions, my husband has the 2x saved. I only have about 1x. lol

Anyway, if you're poor, you're poor and won't have money to save so this advice doesn't really count for you.

I think this advice is more for middle+ class working professionals who don't know what they are doing with their money.

That said, my husband and I are not professionals but we're trying our best and also wasting a bunch of money on the side, but maybe the healthcare situation in the US makes this even more difficult.

You don't get paid for your work? That's what being a professional means, or...?

EDIT: I guess it can be used to describe the opposite of unskilled labor?

Plus bachelors, plus masters, plus interest compounded per annum at 6%

And all said debt in a large, expensive city:

https://www.usnews.com/best-graduate-schools/top-medical-schools/debt-rankings

You're in the top 3% of all U.S. medical students.

Even if we exclude the trust fund babies who got a free ride (the top two groups in the chart above)...

you're still in the top 3% of an infamous group of debtors.

Average pre-med debt is $25,000. You blew by that by over $100,000. The standard 10-year repayment is $2,200 a month for a $200,000 debt at 6% interest rates. You yourself are looking at $5,200 a month, with post-tax money that you cannot deduct on the tax return. Using a generous effective income tax rate of 20%, you're using up $78,000 of your annual salary to be on the standard repayment plan. That's one-third of your total yearly compensation if you decide to become a pediatrician. Your debt will influence your field of choice and where you choose to practice. I hope you have a plan. Taking home <$80,000 a year, less repayments, to slave away as a pediatrician is rough, as an example. Sounds entitled, but it will suck when looking at your peers. Don't bother with becoming a psychiatrist; you'll need one instead. I wish you good luck.

Last edited:

this thread got me thinking so I ran some numbers and realized with the employer match, I'm actually saving more than the 13% of my gross income that I contribute each month and that after accounting for all expenses (based on higher estimate), I should be debt free from student loans in 3.7 yrs! (this all assumes the same salary, which will likely increase by at least 10-15% over the next couple years).

still not satisfied with that solution. I just want this shit goneeee

still not satisfied with that solution. I just want this shit goneeee

You're in the top 3% of debtors.

Average pre-med debt is $25,000. You blew by that by over $100,000. The standard 10-year repayment is $2,200 a month for a $200,000 debt at 6% interest rates. You yourself are looking at $5,200 a month, with post-tax money that you cannot deduct on the tax return. Using a generous effective income tax rate of 20%, you're using up $78,000 of your annual salary to be on the standard repayment plan. That's one-third of your total yearly compensation if you decide to become a pediatrician. Your debt will influence your field of choice and where you choose to practice. I hope you have a plan. Taking home less than $80,000 a year, less repayments, to slave away as a pediatrician is rough, as an example. Sounds entitled, but it will suck when looking at your peers. Don't bother with becoming a psychiatrist; you'll need one instead. I wish you good luck.

Thanks for the heads up. I didn't know my debt was high =p

Income based repayment plans help greatly with repayment. I wish I qualified for the other plan, the pay as you earn plans. They're more generous. For some reason they're limited to borrowers after a certain date though.

Also, your reference showed median. My link showed the variability given region. This is due both to institution tuition and cost of living. For instance, going to Georgetown is incredibly expensive compared to going to school in eastern Washington state.

On your thoughts regarding specialty, pediatricians are among the lowest paid physicians but even they make considerably more than $80k, unless they're working part time. Actually, psychiatrist pay has increased drastically in the last several years and it was one of the highest

To quote Albert Einstein...

"Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it. Compound interest is the most powerful force in the universe."

If you chose to invest, you're earning compound interest.

If you chose debt, you're paying it.

"Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it. Compound interest is the most powerful force in the universe."

If you chose to invest, you're earning compound interest.

If you chose debt, you're paying it.

This whole thing has been amusing to me. With 401K added it's definitely in the realm of possibility for me and I have years to go. Even so, the headline is pretty shit and my wife's friend is the author of the article. She hadn't no control over the headline they picked up, and it's been hell of a thing to see how this has spread. She's going on tv to talk about the article tomorrow even. Small world.

Yeah! Me and husband both just stock groceries on shelves! :DYou don't get paid for your work? That's what being a professional means, or...?

EDIT: I guess it can be used to describe the opposite of unskilled labor?

But the wage is surprisingly decent for unskilled labour if you get full-time (~40k each with pensions too because I assume our union is holding down the fort).

The $80,000 refers to take-home pay, not total salary. Which is what you'll be taking in if you decide to become a pediatrician and after paying off your monthly debt. If $80,000 sounds like enough for you to live near Georgetown or any other HCOL area, go for it. I just think it's very sad that high debt burden influences something that should be a vocation.On your thoughts regarding specialty, pediatricians are among the lowest paid physicians but even they make considerably more than $80k, unless they're working part time. Actually, psychiatrist pay has increased drastically in the last several years and it was one of the highest

The bank owns my house for the next 25 years. ;)Like "I put a 50k down payment on my house so I got nowhere near 2x my salary in savings lul"

This whole thing has been amusing to me. With 401K added it's definitely in the realm of possibility for me and I have years to go. Even so, the headline is pretty shit and my wife's friend is the author of the article. She hadn't no control over the headline they picked up, and it's been hell of a thing to see how this has spread. She's going on tv to talk about the article tomorrow even. Small world.

It has been fidelity's guidance for years. I wonder why it is blowing up now?

It has been fidelity's guidance for years. I wonder why it is blowing up now?

Interesting. Had if a late start due to grad school, but my calculations tell me I should have 24x the salary we have by 60. That's just by maxing a 401k each year.

I initially started typing out a laugh, but the reality is that due to our combined student loan debts and children, there is no way we're even close to that. We've made some changes recently to help with paying down debt, but there is a good bit of forward and back that occurs just because life shit happens, too. What it really boils down to is this. I'll be working forever.

Interesting. Had if a late start due to grad school, but my calculations tell me I should have 24x the salary we have by 60. That's just by maxing a 401k each year.

Once you hit 20x your annually salary there isn't much benefit in working anymore (unless you really like your job of course!) at 20x you can live off investment returns indefinitely without touching the principle.

If you're going to go over that before 60 you should really look into diverting some of that into an HSA if you aren't already.